Best High-Yield Savings Accounts Of 2024

You can grow your money more quickly than with normal accounts with the finest high-yield savings accounts. The items highlighted on this page have 5% or higher annual percentage yields, or APYs. That is significantly higher than the 0.46% national average rate.

The current is a fantastic moment to open a high-yield savings account because of the recent hikes in Federal Reserve interest rates, which are driving up APYs. You can save money for large purchases or increase your emergency reserve with the accounts listed below. For further details on the operation of these financial products, scroll to the bottom of the page.

Why you can trust themoneymail:

To guarantee fairness and truth in our coverage and assist you in selecting the financial accounts that are most suitable for you, our authors and editors adhere to stringent editorial criteria. View our standards for assessing credit unions and banks.

APY research methodology:

As of this page’s publishing date, the APYs displayed are up to date. We check account rates every daily to make sure we have the most recent APYs.

All APYs are up to date as of December 8, 2023. The rest of the data is accurate as of December 1, 2023.

Best High-Yield Savings Accounts

To identify some of the top high-yield savings accounts available, we analyzed 73 online savings accounts offered by 53 nationally accessible banks and credit unions.

Best Online High-Interest Savings Rates

Our ranking of the top accounts took into account a number of factors, not just the annual percentage yield (APY). This is an overview of our best accounts, arranged by highest available APY.

- Milli Savings Account: 5.50% APY

- UFB Secure Savings: Up to 5.25% APY

- Bread Savings High-Yield Savings Account: 5.15% APY

- Bask Interest Savings Account: 5.10% APY

- BMO Alto Online Savings Account: 5.10% APY

- M1 High-Yield Savings Account: Up to 5.00% APY

- Synchrony Bank High Yield Savings: 4.75% APY

- SoFi Checking and Savings Account: Up to 4.60% APY

- Citizens Access® Savings: 4.50% APY

Which High-Yield Savings Account Is Best for You?

Milli Savings Account: Best for Separate Savings Goals

The ideal savings account for anyone pursuing several financial objectives is Milli’s. You may design and personalize up to five distinct savings objectives with Milli Savings Jars. You’ll also receive one of the best savings rates out there.

Bask Interest Savings Account: Best for Simple High-Yield Savings

The Interest Savings account from Bask Bank is a minimal-frills account that offers a competitive interest rate on any balance, no monthly fees, and no minimum balance requirements—if you value simplicity of usage and high interest above a ton of features.

M1 High-Yield Savings Account: Best for High Balances

Customers who intend to maintain a large sum in their savings account can consider M1’s High-Yield Savings Account. Through its network of insured institutions, M1 provides up to $5 million in FDIC coverage, beyond the typical $250,000 per institution covered by FDIC insurance.

UFB Secure Savings: Best for Cash Withdrawals

The ideal account for users who frequently withdraw cash is UFB Secure Savings. Savings accounts rarely come with ATM cards; however, UFB offers a free card and free use of over 91,000 ATMs.

Bread Savings High-Yield Savings Account: Best for Frequent Deposits

If you need to deposit money into your savings account frequently, the Bread Savings High-Yield Savings Account is the perfect option. Bread permits limitless mobile check deposits and ACH transfers, in contrast to certain banks that place a monthly deposit cap. Additionally, inbound wire transactions are free of charge.

SoFi Checking and Savings: Best for Combined Checking and Savings

Customers who conduct all of their banking activities in one account—from spending to saving—benefit greatly from SoFi Checking and Savings. The easy-to-use checking facilities and high interest earnings will appeal to those who value having just one account for convenience’s sake.

Citizens Access Savings: Best for No Fees

For those who desire a savings account with no fees, Citizens Access Savings is the finest option—period. While many online savings accounts don’t impose monthly fees, they do charge for additional services like ATM access or excessive transactions. You may rest assured that Citizens Access is a truly free account because there are no fees or additional expenditures.

Synchrony High Yield Savings: Best for ATM Reimbursements

The greatest high-yield savings account for ATM reimbursements is Synchrony High Yield Savings. In addition to providing an ATM card for easy access to your money, Synchrony will pay up to $5 in monthly out-of-network ATM fees for this account.

BMO Alto Online Savings Account: Best for Unlimited Transfers and Withdrawals

The ideal account for limitless transfers and withdrawals is the Online Savings account from BMO Alto. This account can be a good option if you need unrestricted access to your cash or if you routinely transfer money in and out of savings.

Methodology

Some of the greatest APYs are offered by the accounts on this list. Additionally, they score highly based on our comprehensive set of standards for the Best Savings Accounts of 2023.

Forbes Advisor examined 73 online savings accounts at 53 financial institutions—a mix of credit unions, internet banks, and traditional brick-and-mortar banks—to compile a list of the top savings accounts. Within the categories of APY, fees, minimum requirements, customer service, and digital experience, we scored each account based on 12 data points. Every account on our list is an online account.

The weights given to each category for high-yield savings accounts are as follows:

- APY: 70%

- Fees: 10%

- Digital experience: 5%

- Customer experience: 5%

- Minimum deposit requirement: 5%

- Minimum balance to avoid monthly: 5%

We also took into account any complicated tier structures, prerequisites, or other conditions that needed to be met in order to obtain the APY. Scores were adversely impacted by minimum deposit requirements of $10,000 or more and by high minimum balance requirements to avoid fees. For the savings account to be included on this list, it must be accessible nationwide.

See our article on How Forbes Advisor Reviews Banks to find out more about our editorial process, rating and review methodology.

High-Yield Savings Accounts Rates Today

5.84% is the highest interest rate available for savings accounts today. The trajectory of high-yield savings rates is comparable to that of money market and certificate of deposit accounts. Online banks typically offer the best returns for savers among high-yield savings account offers.

Are Savings Interest Rates Going Up?

Rates on high-yield savings accounts were rising steadily through 2022 and have been rising until 2023. The Federal Open Market Committee’s efforts to combat inflation by gradually raising the federal funds rate—the interest rate at which banks lend money to one another overnight—are mostly to blame for this.

Banks usually follow suit and modify the rates for savings and other deposit accounts in line with changes in the federal funds rate. Banks frequently pay higher rates for deposit accounts as a result of rate increases. According to the FDIC, the national average savings rate rose gradually in 2023 along with the federal funds rate, rising from 0.33% in January to 0.46% in November.

To entice savers, banks could only be prepared to raise rates to a certain extent. High-yield savings rates may eventually level off or even start to decline. Additional decreases in savings account APYs may result from Federal Reserve rate cuts.

How High Will Savings Interest Rates Go?

Nobody can predict with certainty how high savings interest rates will rise in the near future, but a lot will rely on how the federal funds rate performs. The target federal funds rate is currently at its highest point in more than 20 years, ranging from 5.25% to 5.50%.

Before the end of 2023, the Federal Open Market Committee will meet one more time, and the Fed may decide to hike rates for the fifth time this year. Interest rates on savings accounts may increase if there is another rate increase. However, most FOMC participants do not anticipate rates to increase significantly in 2024. By the end of 2024, rates are often projected by the FOMC to be slightly lower.

What Is a High-Yield Savings Account?

An account that gives a greater interest rate than a standard savings account is called a high-yield savings account. High-yield savings accounts are typically offered by online credit unions and banks. These financial institutions can pass on savings to customers in the form of better rates and reduced fees because they typically do not have the overhead expenses or profit-margin requirements of a traditional brick-and-mortar bank.

Although there are a number of factors that affect interest rates, high-yield savings accounts frequently give an annual percentage yield (APY) of 4.00% or higher. Up to 25 times the national average interest on regular savings accounts can be earned with a high-yield savings account.

How Do High-Yield Savings Accounts Work?

A standard savings account and a high-yield savings account function similarly. The main distinction is that regular savings accounts are significantly outperformed by high-yield savings accounts. Compared to traditional brick-and-mortar banks, online banks are more likely to provide high-yield savings accounts due to their lower overhead costs.

Your money is secure while earning interest in both regular and high-yield savings accounts. The top accounts don’t have monthly fees or require a minimum balance to earn interest. In principle, you are free to take out and deposit money whenever you want, although certain banks can have monthly transaction limits. Online banks may permit cash deposits at independent merchant locations and ATM withdrawals; otherwise, you can only conduct electronic transactions.

High-Yield Savings Account Terms To Know

There are a few terms you should be aware of while looking into high-yield savings accounts. Determining the appropriate savings choice can be facilitated by comprehending their meaning.

Annual percentage yield (APY).

When compound interest is taken into consideration, the annual percentage yield, or APY, on a savings account is the interest you could receive on your funds over the course of a year.

Compounding interest.

Interest earned on your previously accumulated interest is known as compound interest. Your principal deposits and the interest you accrue over time are used to compute it.

High yield.

A savings account with a high yield provides an interest rate that is higher than usual.

Minimum deposit requirement.

The amount you must deposit to start a high-yield savings account is known as the minimum deposit requirement. This might only be $1 or even $0. It all depends on the bank.

Monthly maintenance fee.

Some banks charge you a monthly maintenance fee in order to maintain your account open. An online bank has the benefit of not charging monthly maintenance costs when opening a high-yield savings account.

Online bank.

Online banks usually don’t have branches; instead, they function online. Rather, you use mobile banking apps or online browsers to access your money. Moreover, some internet banks provide ATM access.

Are High-Yield Savings Accounts Safe?

In general, high-yield savings accounts are thought to be secure locations to keep your money. You are keeping your money with a bank that is FDIC-insured or a credit union that has NCUA protection when you deposit money into a high-yield savings account.

Banks and other financial institutions that provide high-yield savings accounts take several security precautions to safeguard your financial and personal data. Data encryption, safe data storage, and multifactor authentication are a few examples of these precautions.

Can You Lose Money in a High-Yield Savings Account?

If you are saving at a bank or credit union that is insured by the FDIC, you cannot lose money in your savings account.

Up to $250,000 is insured by the FDIC for each depositor, type of account owner, and financial institution holding an account at a member bank. Deposit accounts at credit union members are similarly covered by the National Credit Union Administration (NCUA).

You won’t lose money in savings up to the permitted limits if your bank or credit union collapses and is insured. There is relatively little chance of ever losing money because bank collapses are rare.

But if interest rates can’t keep up with inflation, you can lose some of the benefit of saving. Your savings amount remains unchanged despite inflation, but the purchasing power of your money decreases.

Online Savings Accounts Fees

Compared to traditional savings accounts, internet savings accounts typically feature less and lower fees. There are numerous online savings accounts that don’t need a minimum balance or monthly maintenance fees.

There is no monthly maintenance cost associated with any of our top selections for online savings accounts—you may choose to forgo the fee by enrolling in e-statements. That being said, there are still certain fees associated with these accounts. For things like paper statements and too many transactions, they might charge. Before opening an account, it’s crucial to read the fine print to make sure you’re informed of any costs, just as with any other account or financial product.

How To Pick a High-Yield Savings Account

It’s not always clear which high-yield savings account is ideal, but comparing accounts will help you make the right decision. Before creating an account, take into mind the following factors.

Interest Rate

The interest rate is arguably the most crucial consideration when selecting a high-yield account. Getting a better interest rate will enable you to accelerate the growth of your money.

Deposit Requirements

There are accounts that have a minimum required to open a new account. To receive interest or prevent monthly fees, you might also need to keep a certain amount in your account.

Account Fees

You may lose interest on your money if you incur fees. To find out if there are any further fees or a monthly service charge associated with your account, consult the fee schedule. If you maintain a specific balance in your account, certain banks will waive fees.

Compounding Frequency

Depending on the bank, interest on a savings account might accrue daily, weekly, monthly, quarterly, or annually. You earn interest on your interest when interest compounds. Over time, you can increase your interest income by selecting an account that compounds more regularly.

Pros and Cons of High-Yield Savings Accounts

Pros

- Higher interest rates than traditional savings accounts

- Lower or no fees

- User-friendly mobile platforms

- Unique savings tools

Cons

- In-person banking may not be an option

- Cash withdrawals and deposits may not be available

- May have requirements you must meet to earn the highest APY

- Interest rates are variable and can change at any time

How To Open a High-Yield Savings Account Online

A high-yield savings account can be opened really rapidly. After determining which account best suits your requirements, you must submit an online application. When you apply, the bank might need some particular information to confirm your identity:

- Name

- Address

- Email address

- Phone number

- Date of birth

- Social Security number

- Number from your driver’s license or other government-issued photo ID

- Funding source account information

Both of you will need to furnish personal and financial information when opening a joint account.

After the account has been approved, you can fund it with funds from another bank account or through other legal means.

Best Ways To Use a High-Yield Savings Account

High-yield savings accounts are great for achieving savings objectives because of their earning potential. You can store the money for your savings objectives apart from your regular spending account by creating a separate account for them. A high-yield savings account can be used to save money for many different purposes, such as:

- An emergency fund

- Upcoming vacations

- A wedding

- Home renovations

- Home furnishings

- A down payment on a home

- A new car

- Educational expenses

High-yield savings accounts are not recommended for storing retirement funds; instead, they are best for short-term financial objectives. Compared to high-yield savings accounts, tax-advantaged retirement or investment accounts usually provide higher returns and tax savings.

Large Expenses

You can utilize high-yield savings accounts to put money aside for a range of significant costs. Among the objectives you may save for are:

- A down payment on a home

- Home renovations or repairs

- A new car or recreational vehicle

- Wedding expenses

- New furniture

Holding your emergency savings in a high-yield account is an additional option. Generally speaking, it’s advisable to have emergency cash in a liquid, immediately accessible account in case you suddenly need money.

Education

You may want to think about opening a high-yield savings account in order to put money aside for your educational costs. Among the costs you could put money aside for are:

- Private school tuition and fees for elementary, middle or high school students

- Extracurricular costs, such as band instruments, travel expenses for competitive sports or class trips

- College tuition and fees

- In-school living expenses, such as meals or rent

A 529 savings plan is a viable alternative to a high-yield savings account if your primary goal is to save money for college. You can invest money for college and take it out tax-free for approved educational costs with a 529 account.

Vacation

Savings accounts with high yields are a desirable option for setting aside funds for trips or holidays. A high-yield account could be used to save money for:

- Flights

- Hotel or resort stays

- Local transportation

- Meals

- Souvenirs

- Entry fees for attractions or experiences

To cover such costs and possibly earn some cash back in the form of travel miles or points, you could utilize a credit card with travel rewards. Nevertheless, the APR on your credit card may negate the value of whatever points you accrue if you wind up carrying a load from month to month.

You might be better off using a high-yield savings account to save money for your vacation plans if you’d rather to earn interest than pay it.

Are High-Yield Savings Accounts Worth It?

If you want to put money aside for immediate needs or objectives, a high-yield savings account is a good way to do it. It’s a fantastic alternative for some savings objectives, but it shouldn’t be used in place of a retirement or tax-advantaged investing account.

An excellent location to keep your emergency fund is, for instance, a high-yield savings account. The money is immediately accessible, but it earns higher interest than it would in a conventional savings account. However, if you had ten years or more to invest, it wouldn’t make sense to retain your child’s college funds in a high-yield savings account.

Alternatives to High-Yield Savings Accounts

Savings shouldn’t just be kept in high-yield savings accounts. Some choices that you may want to think about are as follows:

- Money market accounts

- Certificates of deposit

- Cash management accounts

- Investment accounts

High-Yield Savings vs. Money Market Account

Deposit accounts that combine the capabilities of savings and checking accounts are known as money market accounts. Perhaps earning interest works similarly to how a savings account works. However, you might also be able to use a linked debit card to make purchases or write checks from your account. These are the kinds of things that savings accounts normally don’t offer.

So, which is preferable, high-yield savings or a money market account?

The answer is contingent upon your needs regarding the account, your willingness to pay for it, and the type of annual percentage yield (APY) you hope to achieve. Although there may still be monthly limits on the amount of withdrawals and transfers you can make, money market accounts can provide you with greater freedom and access to your resources. High-yield savings accounts, however, could provide higher interest rates.

High-Yield Savings vs. Certificates of Deposit (CD)

In that you get interest on your balance, certificates of deposit (CDs) and savings accounts are comparable financial products. The main distinction is that funds deposited into a certificate of deposit (CD) are locked up for a predetermined amount of time, such three months or a year. You may lose all or part of the interest you receive if you take your money out of the CD before it matures.

Given that your rate won’t often change during the duration of the CD, higher rates and guaranteed profits are the key advantages of CDs over high-yield savings accounts. Although CDs let you fix an interest rate for a predetermined amount of time, the drawback is that accessing your money is more difficult and expensive. Because of this, if you are certain that you won’t need to access your money until the maturity date, CDs make sense.

Other High-Yield Savings Account Alternatives

CDs.

The finest CDs offer competitive rates, but there’s a time limit on how long you can keep your money locked in. You risk losing all or part of the interest you earned if you take your money out of the CD before it matures.

Cash management accounts.

Cash accounts are meant to retain money that you want to invest later or that you receive after selling investments that you own. They are typically linked to taxable brokerage accounts. Like a savings account, a cash account can be used to earn interest at rates that are competitive with those of a checking account.

Investment accounts.

The purpose of these accounts is to facilitate financial market investments. Compared to a savings account, a brokerage account may provide a significantly higher return, but there is a chance of losing money.

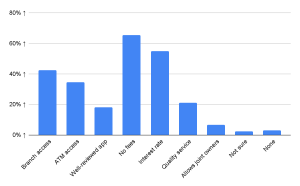

Americans’ Considerations When Comparing Savings Accounts

In a OnePoll-conducted Forbes Advisor study, participants were asked to rank the top three attributes that they look for in a new savings account.

The two most common complaints were fees (65%) and interest rates (55%), with branch access (42%) and ATM availability (35%).

In compliance with the code of conduct of the Market Research Society, OnePoll, a market research firm, was tasked by Forbes Advisor with conducting an online poll of one thousand American adults (18 years of age or older) who own at least one bank account (checking or savings). From November 9 to November 13, 2023, data was gathered. With 95% confidence, the margin of error is +/- 3.1 points. The OnePoll research team, a corporate member of the American Association for Public Opinion Research (AAPOR) and a member of the MRS, was in charge of this poll.

Recap: Best High-Yield Savings Accounts Of 2023

- Milli Savings Account: 5.50% APY

- UFB Secure Savings: Up to 5.25% APY

- Bread Savings High-Yield Savings Account: 5.15% APY

- Bask Interest Savings Account: 5.10% APY

- BMO Alto Online Savings Account: 5.10% APY

- M1 High-Yield Savings Account: Up to 5.00% APY

- Synchrony Bank High Yield Savings: 4.75% APY

- SoFi Checking and Savings Account: Up to 4.60% APY

- Citizens Access® Savings: 4.50% APY

Getting a high-yield savings account can be a wise choice if you want to earn a competitive rate and keep your money safe. You can choose the finest high-yield savings account for your needs by comparing rates offered by credit unions, traditional banks, and online banks.

Banks We Monitor

When looking for the greatest high-yield savings account rates, we considered the following institutions:

Affirm, Alliant Credit Union, Ally Bank, American Express, Axos Bank, Bank of America, Bank5 Connect, BankDirect, BankPurely, Barclays, Bask Bank, BrioDirect Banking, Capital One, Charles Schwab Bank, Chase, Chime®, CIBC Bank, CIT Bank, Citibank, Citizens Access, Colorado Federal Savings Bank, Bread Financial, Connexus Credit Union, Consumers Credit Union, Discover, Dollar Savings Direct, E*Trade Bank, Fitness Bank, FNBO Direct, HSBC, HSBC Direct, iGoBanking, Incredible Bank, Live Oak Bank, Marcus by Goldman Sachs, My eBanc, MySavingsDirect, Navy Federal Credit Union, nbkc Bank, PNC Bank, Popular Direct, Purepoint Financial, Quontic, Rising Bank, SalemFiveDirect, Sallie Mae Bank, SFGI Direct, SmartyPig Bank, Synchrony Bank, U.S. Bank, UFB Direct, Varo Bank and VIO Bank.