14Common Bank Fees and How to Avoid Them

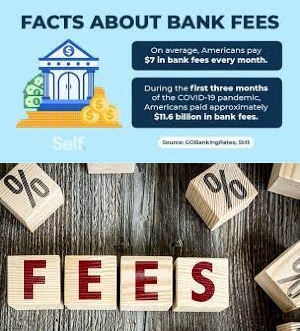

According to a Bankrate survey from 2023, more than 25% of Americans with checking accounts pay an average of $24 in banking fees each month. These fees vary by user, however, they range from monthly maintenance/service fees to charges for overdrafts and insufficient money. While a few dollars here and there may appear insignificant, they may certainly build up over time.

In just a year, $24 a month would deplete the average consumer’s savings account balance of $288. The good news is that you can easily avoid bank fees if you are aware of them ahead of time. You can look around for solutions with lower fees, and we’ll make some recommendations later.

Themoneymail Select breaks down the most frequent banking fees and how to avoid them, which can save you hundreds of dollars over time.

- Monthly maintenance/service fee

- Out-of-network ATM fee

- Excessive transaction fee

- Overdraft fee

- Insufficient fund fee

- Wire transfer fee

- Early account closing fee

Bank fees are rather prevalent. Fees charged by banks, such as ATM fees, account maintenance costs, overdraft fees, stop payment fees, and so on, can quickly pile up. That’s money better spent or saved in your savings account.

If you see bank fees listed on your monthly bank account, you’ll be relieved to know that there are various ways to reduce or eliminate these additional charges. Here are seven frequent banking fees and ways to avoid them.

1. Monthly Maintenance Fee

Many banks charge a monthly fee to retain your money in an account with them. Monthly fees can range between $4 and $25, but they are typically easy to avoid. Account holders can avoid monthly fees by opening a checking and savings account at the same bank or keeping a minimum balance in their account. Sometimes, setting up a monthly direct deposit is enough to waive the monthly cost.

However, you can open a checking or savings account with no monthly fees from the start. Themoneymail Select reviewed the finest no-fee checking accounts, and Capital One 360 Checking was named best overall for its top-rated mobile app, physical bank facilities, and customer service.

The money you save by not paying any monthly fees can instead earn you more in a high-yield savings account that offers no fees at all, such as the LendingClub High-Yield Savings account.

How to avoid it:

Choose your account carefully. Ask your bank if they impose a monthly maintenance fee and what the circumstances are for waiving it. If you satisfy the minimum balance requirements or make a particular amount of purchases from your account each month, you may be able to avoid this fee completely.

2. Out-of-network ATM fee

ATM fees from both your bank and the ATM operator can mount up if you withdraw cash frequently. The big brick-and-mortar banks charge consumers an average of $2.50 to use a non-network ATM. Use only ATMs inside your bank’s network, which are usually listed on their website. Most banks’ mobile apps assist consumers in locating and using the nearest fee-free ATMs.

If you’re in a hurry and can’t find an in-network ATM, withdraw a greater amount so the cost is only one time, or try to get cash back by using your debit card at your next purchase.

Some banks may grant a refund for out-of-network ATM provider fees. For example, Synchrony Bank in the United States refunds up to $5 in ATM fees per statement cycle. Still, be cautious about how much you withdraw from an ATM because the costs, even with a $5 refund, can quickly add up. According to Bankrate, out-of-network ATM operators charge clients an average of $4.73. In some circumstances, even going to the ATM twice in a month will exceed the recoverable amount.

How to avoid it:

If you must make a withdrawal from an out-of-network ATM, try to withdraw a bigger amount of cash to avoid incurring multiple transactions in a short period and paying more costs than necessary. “Like any financial service, it’s important for consumers to understand account terms,” Greene said. “ATM fees are generally waived, for example, if the ATM is within the network, and some institutions offer waivers or refunds out of network as well.”

3. Excessive transaction fee

An excess transaction fee is incurred when savings account customers withdraw more than the federal limit of six free withdrawals and transfers each month. It should be noted, however, that this limit is now lifted under Regulation D due to the coronavirus outbreak.

Excessive transaction costs can range from $3 to $25 per transaction, but you can easily avoid them if you use your checking account for normal withdrawals, such as paying bills.

4. Overdraft fee

Overdrawing your bank account is a simple mistake. To avoid this, set up direct deposit so that money is consistently and automatically deposited into your account. This will allow you to keep the minimum balance required for your account and avoid overdrafts.

Many banks also charge a fee for overdraft protection, which typically costs $35 per overdraft. Instead of declining a purchase because you do not have enough money in your bank account, the bank will cover you by withdrawing funds from your connected savings account, second checking account, line of credit, and so on.

How to avoid it:

Set up account alerts to receive notifications every time you purchase with your card or when your balance falls below a specific amount. That way, you’ll always have enough money in your account to make purchases.

Another alternative is to ask your bank if they offer overdraft protection. When you enroll, your bank will transfer funds from a linked or secondary account to your account to cover the purchase. This option will most likely require you to pay a monthly charge, but investing a few dollars each month to ensure that any purchases that cause your account to fall below zero are still approved and do not result in an overdraft fee could help you save.

5. Insufficient fund fee

For people who do not use overdraft protection, inadequate funds can be costly while making a purchase. An inadequate fund or returned-item fee for failed transactions can be up to $35 per transaction. These fees, as well as bounced check fees, can be avoided by monitoring your account and sending funds ahead of time. Sign up for notifications to receive automatic text or email alerts when your balance is low. In this manner, you can be confident that your cash will cover you.

How to avoid it:

Tracking your expenditures, setting balance alerts, and enabling overdraft protection may help you avoid insufficient money costs.

6. Wire transfer fee

Wire transfers are a quick and convenient way to send money without using real cash, but they come with a fee. Banks normally charge between $16 and $35 for every domestic and international transfer. Use wire transfers sparingly, unless it is an official transaction involving a large sum of money. Alternatively, you can transfer funds online or via your bank’s mobile application.

How to avoid it:

Some financial institutions will waive or lower this cost if you transmit the money online rather than contacting a customer service agent. Consider transferring funds via a physical check or a mobile payment app such as Venmo or Zelle.

7. Early account closing fee

Closing your account too early has consequences. Banks have varied schedules (typically 90 to 180 days) for how long you can keep your account active before terminating it without incurring a fee, which can reach $25. Before you terminate your account, make sure you understand your bank’s rules.

How to avoid this fee:

Although there is no certain way to prevent your written checks from being stolen or misplaced, you can reduce the likelihood of this happening by paying your bills online or taking your checks to a local post office rather than leaving them in your mailbox. When writing a check, make sure the funds are in your account and that it is made out to the correct recipient. You should also move promptly to halt payment before the transaction goes through or the check is cashed.

8. Account closing fees

Some banks will charge you an account closing fee if you close your account within a particular time frame after opening it. This is done to retain customers or to dissuade new customers from taking advantage of initial offers and then switching to another bank. Most financial institutions impose this fee if you close an account that is less than 180 days old, however some have lower time frames.

How to avoid it:

Before opening an account, ensure that the bank you choose fulfills your long-term needs. If you decide it isn’t for you, attempt to remain around after the cutoff date to avoid paying an account closure fee.

9. Dormancy fees

When your account becomes dormant, banks have a limited amount of time to encourage you to use it before the government intervenes and has the authority to decide what happens to the funds in your account. Banks often charge a dormancy fee after your account has been inactive for at least six months.

How to avoid it:

Consider making regular deposits and withdrawals from this account. You can also set up one of your monthly recurring payments from this account to keep it open and operational, even if you don’t use it often. If you discover that you do not need the account, consider closing it to avoid incurring excessive monthly inactivity costs.

10. Foreign transaction fees

A foreign transaction fee is likely to be charged whenever you purchase from an international retailer, whether online or overseas. This cost is split between your credit card issuer and your credit card network and is calculated as a modest percentage of your total transaction, often 1% to 4%.

How to avoid it:

Not every bank charges overseas transaction fees. However, if you travel frequently or buy online, it may be worthwhile to create a new account with a bank such as Capital One or HSBC, both of which remove international transaction costs when you use specified goods to pay for your purchases.

11. Lost card fees

We’ve all been guilty of losing or misplacing our bank cards. However, if you lose track of yours, you may have to pay a price to have it replaced, as well as an additional fee to have it replaced on time.

How to avoid it:

Ask your bank whether they are willing to forgo the replacement fee. If this is your first time losing your card or if your card was stolen, your bank may be willing to make an exception. If you can’t avoid the replacement price, you can save money on having your card expedited by choosing the usual processing and shipping time and utilizing a mobile wallet or cash for a few days while you wait for your new card to arrive.

12. Stop Payment Fee

If you believe a check you wrote has been lost or stolen, was sent to the incorrect address, you have insufficient funds in your account, or there is a dispute over a purchase, contact your bank and place a stop payment on the check so it is not paid or cashed by your bank.

This might also apply to ACH payments, such as recurring monthly bill payments. Remember that to stop an ACH payment, you must contact the bank (by phone or in writing) at least three days before the planned transfer date. Many banks charge a fee for this service, which varies but is often around $30.

How to avoid this fee:

Although there is no certain way to prevent your written checks from being stolen or misplaced, you can reduce the likelihood of this happening by paying your bills online or taking your checks to a local post office rather than leaving them in your mailbox. When writing a check, make sure the funds are in your account and that it is made out to the correct recipient. You should also move promptly to halt payment before the transaction goes through or the check is cashed.

13. Check Fees

Although the majority of consumers pay their bills electronically, some businesses and individuals may not have an account that permits them to receive online bill payments and must instead accept physical checks. Alternatively, rather than risk sending money via mail, you may write a check to a person for their birthday or another occasion and include it in their card.

Some banks impose a fee for each check you write, or for writing more than a specific number of checks per month. If you order your checks through your bank, you will most likely be charged a check printing fee, which is withdrawn automatically from your checking account. Cashier’s checks cost between $5 and $15.

How to avoid these fees:

Paper check rates vary depending on the form of check you choose and how many you write each month. Some account types provide free standard check styles or savings on nonstandard styles. You can cut this expense by paying as many bills online as possible or sending money to friends and family using a payment platform or app. You might want to order your checks from a company that specializes in paper checks and can provide lower costs than most banks.

14. Paper Statement Fee

Receiving a monthly statement in the mail used to be the only option to acquire information about the previous month’s transactions. In today’s era of online and mobile banking, statements are emailed to customers or made available on the banking app or website, allowing users to access all of their banking information at any time.

However, some consumers prefer to get hard copy statements in the mail rather than via email or online. Unfortunately for people who prefer paper, some banks charge a fee to print and mail statements. These costs might cost you up to $3 each month, depending on your bank.

How to avoid this fee:

Paper statement fees are not going away, as they represent banks’ attempts to convince their consumers to accept e-statements. It costs banks more money to create paper statements than electronic statements, so they pass that expense on to customers.

Signing up for paperless banking will eliminate this fee, but there is no way to receive print statements without paying a fee unless your bank charges none.

What are bank fees?

Bank fees are any fees charged by your bank for conducting business with them. Common fees include ATM fees, paper statement fees, and overdraft fees, among others. When considering opening an account with a new bank, you should research its website or even visit a branch in person to learn about all of the potential expenses.

According to Consumer Finance Protection Bureau data from 2019, bank revenue from overdrafts and non-sufficient funds (NSF) was anticipated to be $15.47 billion.

“For some banks, fees can be a significant source of revenue, however, the proportion varies greatly by institution. Meghan Greene, senior director of research at Financial Health Network, adds that they can also help to reduce operating costs. “It is rather normal to be charged one of these fees. According to our nationally representative FinHealth Spend study, 49% of banked households reported paying a fee for their bank accounts in 2021.”

What are 10 bank fees?

- Monthly maintenance/service fee. This is a fee that banks charge to cover the cost of maintaining your account each month.

- Out-of-network ATM fees.

- Overdraft fees.

- Insufficient funds fees.

- Paper statement fees.

- Wire transfer fees.

- Account closing fees.

- Dormancy fees.

How can you avoid bank fees?

- Utilize free checking and savings accounts. Many banks still offer them.

- Sign up for a direct deposit.

- Keep a minimum balance.

- Keep multiple accounts at your bank.

- Use only your bank’s ATMs.

- Don’t spend more money than you have.

- Sign Up for Email or Text Alerts.

What are 3 fees that can be charged at a bank?

Bank fees include account maintenance charges, withdrawal and transfer fees, automated teller machine (ATM) fees, non-sufficient fund (NSF) fees, late payment charges, and others.

In Conclusion

Although bank account fees are widely accepted, a recent American Bankers Association (ABA) poll of persons over the age of 18 revealed that the vast majority of Americans pay little or no monthly bank fees. If your bank charges fees for overdrafts, stopping payments, using ATMs, or for any other reason, you may be able to reduce or eliminate them. This will allow you to put more money into your emergency fund, down payment funds, or simply enjoy a nice vacation.

The Experian Smart Money™ Digital Checking Account & Debit Card helps develop credit without debt by automatically linking to Experian Boost®ø, which provides credit for qualified bill payments. Experian Smart Money offers no monthly fees, access to over 55,000 fee-free ATMs worldwide**, and direct deposit for up to two days early paychecks†. Get an Experian Smart Money Account with a free or premium Experian subscription, which includes access to your FICO® Score☉, credit report, and more. See the terms at experian.com/legal.