10 Best Checking Accounts of 2024

The finest checking accounts minimize friction by making it simple to access and spend your money at any time and from any location. Take your needs and habits into account when looking for the ideal checking account for you. The top checking accounts are outlined here, along with what makes each unique.

Best Checking Accounts 2024

As of November 2023, the average interest rate on a checking account nationwide is 0.07% APY, as reported by the FDIC. While checking accounts at traditional banks typically yield minuscule interest rates, many Internet banks offer rates that are up to 100 times higher than the national average.

To identify some of the greatest choices, we have evaluated 157 checking accounts offered by 66 banks and credit unions across the country. See below for specific bank assessments, the reasons behind our selection of each account, and the advantages and disadvantages.

The account information and annual percentage yields (APYs) are current as of December 14, 2023.

Methodology

Forbes Advisor examined 157 checking accounts at 66 financial institutions—a mix of conventional brick-and-mortar banks, internet banks, and credit unions—to compile this ranking. Within the categories of costs, access, customer experience, digital experience, minimums, and APY, we scored each account based on 17 data points.

The weighting given to each category is as follows:

- Fees: 50%

- Branch and ATM access: 15%

- Customer experience: 10%

- Digital Experience: 10%

- Minimums: 10%

- APY: 5%

Monthly fee, ability to waive monthly fee, overdraft fee, NSF fee, other fees, ATM network, branch access, Better Business Bureau rating, Trustpilot rating, live chat availability, mobile app ratings, online bill pay availability, online banking access, minimum deposit requirements, and minimum balance requirements were some of the specific features taken into consideration within each category.

The best-scoring checking accounts were those with minimal prerequisites, no fees, or extremely low costs along with excellent ratings for customer service and digital experience. The checking account must be accessible across the country to be listed.

Complete Guide to Checking Accounts

- Current Highest Interest Rates on Checking Accounts

- What Is a Checking Account?

- Types of Checking Accounts

- Checking Account Fees

- Checking Account Bonus Offers

- Pros and Cons of Checking Accounts

- Do Checking Accounts Earn Interest?

- How To Choose a Checking Account

- What Do You Need to Open a Checking Account?

- Checking vs. Savings Accounts

- Most Americans Have Never Switched Checking Accounts

- Banks We Monitor

- Recap: Best Checking Accounts

- Frequently Asked Questions (FAQs)

Current Highest Interest Rates on Checking Accounts

As of December 12th, 2023, 7.72% is the highest average interest rate on a checking account that Curinos has ever recorded. This high rate has not decreased since the middle of September.

What Is a Checking Account?

A checking account is a kind of deposit account that gives you convenient access to your money at all times and the flexibility to deposit and withdraw as much as you like. A checking account can be used for making purchases, paying payments, and handling other day-to-day financial activities. Credit unions, internet banks, and physical banks can all accept the opening of these accounts. They are made to be used daily and to store money for upcoming expenses.

How Does a Checking Account Work?

The purpose of checking accounts is to save money for regular transactions and unforeseen expenses. Usually, they include a debit card that may be used for ATM withdrawals, payments, and purchases. When it comes to withdrawals, checking accounts are often less constrictive than savings accounts; nonetheless, the daily amount that you can take out of an ATM or spend with your debit card may be restricted by your bank.

Although the majority of checking accounts are interest-free, more banks are increasingly providing checking accounts with interest. To keep your checking account open, your bank might charge a monthly maintenance fee. Alternatively, it might waive the price provided you maintain a certain amount of money in the account.

How Much Money Should You Keep in a Checking Account?

There is no standard amount that you should maintain in your checking account because every person’s financial circumstances are unique. However, to cover unforeseen expenses, it’s generally a good idea to have one to two months’ worth of living expenses in your bank account.

To determine how much money you should have in your account each month, keep a record of your monthly spending. In case of an emergency, having an additional financial reserve will help you remain ready.

How Old Do You Have To Be To Open a Checking Account?

Generally speaking, you have to be at least 18 years old to open a personal checking account. Nonetheless, a parent or legal guardian may add a minor as a co-owner to numerous bank accounts. Although there are possibilities for younger children as well, most joint checking accounts require co-applicants to be at least 13 or 14 years old to be eligible.

For children and teenagers, teen checking accounts are the ideal option. Compared to regular joint accounts, several have significantly lower minimum age requirements—some allow users to apply as early as six years old. These joint checking accounts frequently come with extra security features like spending limits on debit cards and parental controls.

Types of Checking Accounts

To satisfy different banking demands, there are several kinds of checking accounts available, such as:

Traditional checking account:

A traditional or normal checking account includes a debit card for purchases and ATM withdrawals, and it allows you to do basic expenditure tasks like writing checks.

Premium checking account:

Improved banking services are included with premium checking accounts. You might have to fulfill greater balance or deposit criteria, or you might have to pay a monthly access charge, depending on the bank. As your balance increases, premium accounts typically provide more alluring features.

Interest-bearing checking account:

Certain checking accounts are entitled to interest, as the name implies. Additionally, the selection of high-yield checking accounts is expanding. To earn interest, banks that provide these accounts frequently have balance requirements.

Rewards checking account:

Like a credit card, rewards checking accounts allow you to accrue points for your purchases. This usually means that every debit card purchase will result in cash back.

Student checking account:

Teenagers and college students who want to open their first checking account are the target audience for student checking accounts. Overdraft protection and minimal or no fees are common features of these accounts.

Second-chance checking account:

People with a bad credit history might be able to open a second-chance checking account. These accounts typically have monthly costs that are inescapable.

Business checking account:

Owners of businesses can use these accounts to track costs, make tax preparation easier, and keep their personal and corporate finances separate. In addition to giving you access to merchant services like credit card processing, business checking accounts can assist you in building a credit history for your company.

Senior checking account:

For those 55 years of age and above, this kind of account usually comes with free checks, no monthly fees, and penalty-free emergency early withdrawals on CDs.

Checking Account Fees

The most optimal checking accounts have low costs. It’s useful to take into account the following typical checking account fees when comparing checking accounts:

- Monthly maintenance fees

- Paper statement fees

- Wire transfer fees

- Out-of-network ATM fees

- Foreign ATM fees

- Foreign transaction fees

- Overdraft fees

- Returned item (NSF) fees

- Cashier’s check, certified check, and money order fees

If you meet specific standards, many banks will waive your monthly maintenance fees. For instance, you can be required to keep a minimum average balance or get a specific amount of direct deposits each month.

In addition to frequently having no monthly costs, online banks may also provide benefits like overdraft protection and ATM fee refunds. Fees for international ATM transactions and wire transfers may be less with an online checking account than they would be with a regular bank checking account.

Checking Account Bonus Offers

When you open an account and fulfill specific requirements, such as setting up direct deposit or using your debit card to make a particular number of purchases within the first 90 days, some banks will give you a checking account bonus, which is free cash.

Several checking account bonuses are currently available at both traditional and internet banks, with the potential to earn hundreds of dollars. For accounts with minimal or no monthly fees, the prerequisites for the best bank bonuses are simple to fulfill.

Pros and Cons of Checking Accounts

The most popular kind of bank account for regular use is a checking account. While using a checking account has many advantages, there are also some drawbacks to take into account.

Pros

When you need money, checking accounts make it simple to get it.

Paychecks can be deposited immediately into your account with direct deposit.

Depositors, account ownership types, and financial institutions are all covered up to $250,000 for checking accounts at banks and credit unions.

Cons

Checking accounts may have monthly fees or conditions to stay out of trouble.

The majority of checking accounts have no interest.

Overspending in your checking account may hinder your attempts to conserve money.

Do Checking Accounts Earn Interest?

Since checking accounts are designed to be used often, they typically don’t yield interest. Because of the account’s liquidity, those who do offer interest often have lower APYs than savings accounts. Remember that APYs are subject to change at any time.

Checking accounts that pay interest frequently have minimum conditions that must be fulfilled every statement cycle to receive the yield. These may be keeping a specific minimum balance in your account or completing a specific amount of debit card transactions each month. Before opening an interest-bearing account, make sure you comprehend its terms.

How To Choose a Checking Account

There are numerous checking accounts available, and selecting one isn’t always simple. When looking for a new checking account, keep the following in mind:

Fees.

Fees should be kept to a minimum because daily transactions will be made through a checking account. Be cautious of overdrafts, monthly maintenance, and out-of-network ATM costs. Choose a bank or credit union that maintains low fees by taking a look at your banking practices to determine which fees are most important to you.

Minimums.

To start a checking account, you may need to deposit a minimum amount with certain banks and credit unions. To qualify for the APY and prevent fees, they could additionally need you to maintain a specific minimum balance. Make sure you can meet the requirements of the bank or credit union before opening an account. Alternatively, search for an account with absolutely no minimal prerequisites.

APY.

Certain checking accounts do not offer interest. However, when looking for an account, consider the APY if you want to earn interest on your funds.

Customer service.

It’s crucial to have the ability to contact a customer support agent if an issue or query comes up, whether you bank in person or online. It’s also critical that they respond and are helpful.

Digital experience.

Seek out banks and credit unions with cutting-edge online and mobile banking technology, particularly if you frequently bank online or through a smartphone app.

Safety.

Verify whether your bank account is insured by the Federal Deposit Insurance Corporation (FDIC). In the case of a bank failure, it offers up to $250,000 in insurance per depositor, per bank, for each category of account ownership. In credit unions, look for insurance offered by the National Credit Union Administration (NCUA).

Your banking practices should also be taken into account when determining which checking account features are most relevant to you.

If you frequently find yourself overdrawing your account, consider opening a checking account that waives overdraft fees. Select an account with a well-regarded mobile app if you enjoy banking while on the go. You may choose the ideal checking account for you based on your habits.

What Do You Need to Open a Checking Account?

You may open a checking account online at a lot of banks and credit unions. You must apply in person at a nearby branch for the others. Your bank will want personal information from you, such as your: to validate your identity and eligibility.

verify your identity and confirm eligibility, your bank will ask you to provide personal information, including your:

- Full name

- Physical address

- Driver’s license or other government-issued photo ID

- Social Security number

Generally, if your application is accepted, you can fund the account with cash, a check, or a transfer from another account. However, cash deposits are often not supported by online checking accounts.

How To Open a Checking Account Online

The process of opening a checking account online is the same as it is offline.

Once you’ve selected the ideal checking account, apply online at the bank or credit union and send in the necessary paperwork. You ought to be able to fund your new checking account online after that.

Transferring funds from your existing account may be the easiest way to make your first deposit when creating a checking account at a bank where you already have an account. You will need to provide your bank account and routing numbers to link your existing account when opening a checking account at a new bank. After that, you can move money from your previous account to your new one.

When establishing an online checking account, take into account the first deposit required. A typical bank may require $25, $50, $100, or more to create a checking account. On the other hand, opening deposits for online banks can be as low as $1 or, in certain situations, $0.

How Many Checking Accounts Can I Have?

You can have an infinite number of checking accounts. You can open several checking accounts at several banks or the same bank.

Depending on how you handle your finances, having multiple checking accounts may be wise. For example, if you’re married, you may pay bills jointly with your spouse using a joint account in addition to the one you have in your name. When working for themselves, a self-employed person could keep separate checking accounts for company and personal purposes.

Think about the fees associated with each checking account you open before opening further ones. It would be best if you could locate a free checking account choice that has no monthly maintenance fees. Think about how you’ll monitor your accounts as well. One easy approach to checking your balances in one location is to use a money management or budgeting tool that connects to all of your accounts individually.

Checking vs. Savings Accounts

Savings accounts are meant to be used for money management, whilst checking accounts are mainly utilized for regular spending. The following are some notable distinctions between the two:

Purpose.

Spending is done through checking accounts. Saves are made with savings accounts.

Withdrawals.

With checking accounts, withdrawals are often limitless. Typically, savings accounts only allow six withdrawals per month.

Features.

Debit cards, paper checks, overdraft protection, and other spending services are typically included with checking accounts. Certain savings accounts offer features other than just interest to assist you in saving money.

Interest.

It is not typical for checking accounts to pay interest. However, some do. In most cases, savings accounts do offer interest.

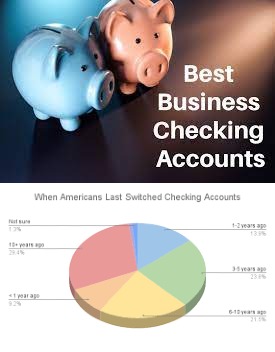

Most Americans Have Never Switched Checking Accounts

Over half (52.0%) of Americans with bank accounts who are banked have never transferred their checking account to a different financial institution, per a Forbes Advisor poll. That’s unexpected given how crowded the checking account market has grown. Among other benefits, a lot of the greatest checking accounts available today allow you to get cash back on purchases, accumulate interest, and receive early direct payments.

29.4% of Americans had moved their money between checking accounts more than ten years ago, followed by 21.5% who did so between six and ten years ago and 23.8% who did so between three and five years ago. 9.2% of Americans switched checking accounts in the last year.

Banks We Monitor

Data from the following financial institutions served as the foundation for our investigation:

Recap: Best Checking Accounts

- Axos Bank Rewards Checking: Best Overall Bank Checking Account

- PenFed Credit Union Access America Checking: Best Overall Credit Union Checking Account

- Discover Cashback Debit Checking: Best Checking Account for Cash Back

- EverBank Yield Pledge Checking: Best Checking Account for Purchase Protection

- nbkc bank Everything Account: Best for Combined Checking and Savings

- Quontic Bank High-Interest Checking: Best Checking Account for Earning Interest

- Citibank Access Account Package: Best for Big Bank Checking

- Varo Bank Account: Best Checking Account for Early Access to Funds

- Connexus Credit Union Xtraordinary Checking: Best Checking Account for Earning Dividends

- Alliant Credit Union High-Rate Checking: Best Credit Union for Digital Banking